The conversation surrounding real-time payment systems is evolving quickly, and nowhere is this more evident than in the dynamic between RTP (Real-Time Payments) and FedNow, two significant players within American payments.

To learn more about these and about the payments space in general, Trade Finance Global (TFG) spoke with Deepa Sinha, Vice President of Payments and Financial Crimes at the Banker’s Association for Financing and Trade (BAFT).

Two payment systems, one goal

Why is a discussion around payment systems even relevant? As Sinha summarised, “There is no trade without payments.”

Real-time payment (RTP) systems represent a modern financial infrastructure designed to enable near-instantaneous money transfers between banks and financial institutions. These systems allow funds to be sent, received, and settled within seconds, 24/7, compared to the historical multi-day processing times of legacy banking systems. While primarily developed in the US, RTP technologies are increasingly gaining global traction.

Operated by a private entity, RTP has established itself among larger banks and financial institutions, building a network with extensive coverage. However, it has faced challenges with limited adoption from smaller institutions, mainly due to technical and financial requirements.

And then there is FedNow, which is backed by the Federal Reserve, and specifically designed to bridge this gap. It aims to serve smaller banks, credit unions, and financial entities that previously found RTP challenging to access due to costs or technological barriers. This resource could level the playing field, ensuring that real-time payments are within reach no matter the size of the institution.

Sinha said, “The coexistence of both RTP and FedNow could serve complementary segments, broadening the reach of real-time payments across various financial institutions, from large banks to smaller community banks and credit unions.”

While their methods and audiences may differ, their respective goals are inherently similar: to provide a faster, more accessible way for institutions and consumers to move money. Two payment systems striving for similar outcomes create an environment of competition—hopefully, a case of healthy competition that drives progress.

Sinha said, “Competition and innovation could encourage both networks to offer unique features or partnerships, and that would enhance the US payment systems competitiveness with international real-time payment networks.”

The introduction of FedNow challenges RTP to do more—perhaps lowering costs or expanding services to remain competitive. In sheer numbers, FedNow is leading: as of July 2024, more than 800 financial institutions across the US have adopted FedNow, compared with 570 on RTP.

With this, FedNow must demonstrate that it can effectively provide value to smaller institutions and address unmet needs. While two-thirds of banks aren’t signed up to RTP or FedNow, the demand is there: 63% of US corporate bankers experience significant or overwhelming demand for instant payments from their corporate customers.

The pressure to innovate is pushing both systems to introduce new features, explore unique partnerships, and strive for efficiencies that might only have been possible with the presence of a competitor. The October 2024 G20 roadmap identified the significant potential held by instant payments in making cross-border payments faster, easier, and cheaper; healthy competition between RTP systems could give rise to excellent options for businesses and consumers.

Building bridges, not walls

Yet, the story of RTP and FedNow is not just about competition; it’s also about collaboration, ultimately through interoperability. For RTP and FedNow to succeed, they must eventually learn how to communicate with one another.

Sinha said, “While RTP and Fed now use similar ISO 20022 standards, full interoperability could be complex and might take time to achieve. The two can definitely coexist, though. If interoperability is prioritised, banks could seamlessly move transactions across both networks, potentially allowing payments initiated in one network to be completed in another.”

ISO 20022 is a global standard that provides a universal language for financial services messaging, creating a common framework for exchanging payment information across different systems. By adopting this standard, RTP and FedNow are using a shared “dictionary” that potentially makes communication between networks easier, though full interoperability remains complex.

This collaboration is easier said than done. While both systems use similar standards, achieving true interoperability is complex and requires considerable coordination and compromise. But it’s worth it. If RTP and FedNow manage to bridge their systems effectively, it would mean a more resilient payment infrastructure for all users.

Payments in a changing world

But this story doesn’t end with interoperability or competition, and it extends far beyond the US borders. As the payments landscape evolves, stakeholders cannot ignore the global context.

With the rise of new alliances like BRICS and the exploration of alternative systems to Swift, payments are transforming worldwide. The development of RTP and FedNow is part of this larger narrative. It’s about positioning the US payment systems to be competitive globally while addressing domestic needs.

Just as speed is essential, so too is the financial system’s integrity. In a world where criminals, from money launderers to fraudsters, are constantly looking for weaknesses, providing fast, secure, and transparent payment options has become crucial to financial security. Innovations such as fraud prevention tools, regulatory frameworks, and enhanced financial inclusion lie at the core of these efforts.

Sinha said, “We’re fighting money laundering, fraud, human trafficking, arms smuggling, drug trafficking. All of these are a profound detriment to the peaceful function of our societies and communities.”

Regulatory frameworks have emerged as critical defenders in this evolving digital payments ecosystem. Standards like the Payment Card Industry Data Security Standard (PCI DSS) provide robust requirements for safeguarding financial data, mandating encryption, regular security assessments, and comprehensive compliance reporting. The EMVCo‘s global payment security standards have been particularly effective, reducing worldwide payment fraud by establishing stringent protocols for card and mobile transactions.

.

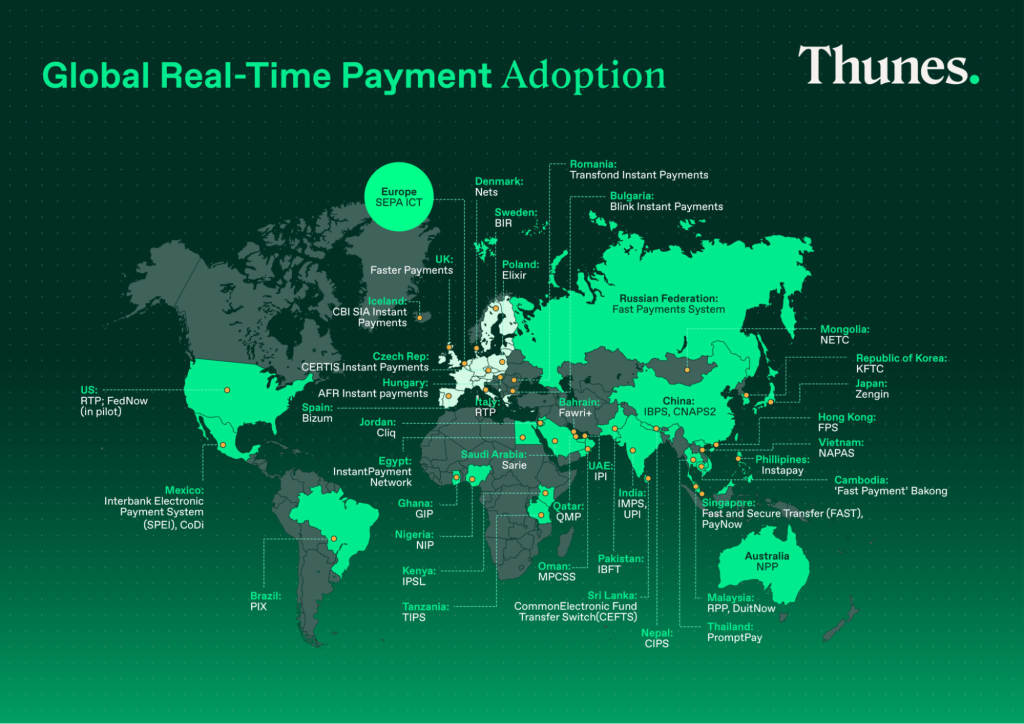

Internationally, Japan pioneered real-time payment processing with its Zengin system in 1973, (though it only became a 24/7 service in 2018). Currently, over 70 countries across six continents support real-time payments. In 2022, the number of transactions reached 195 billion, representing a remarkable 63% year-on-year growth, per ACI Worldwide’s March 2023 report.

India leads the market, processing 89.5 billion transactions through its Unified Payments Interface, launched in 2016. Brazil, China, Thailand, and South Korea follow as significant real-time payment markets.

—

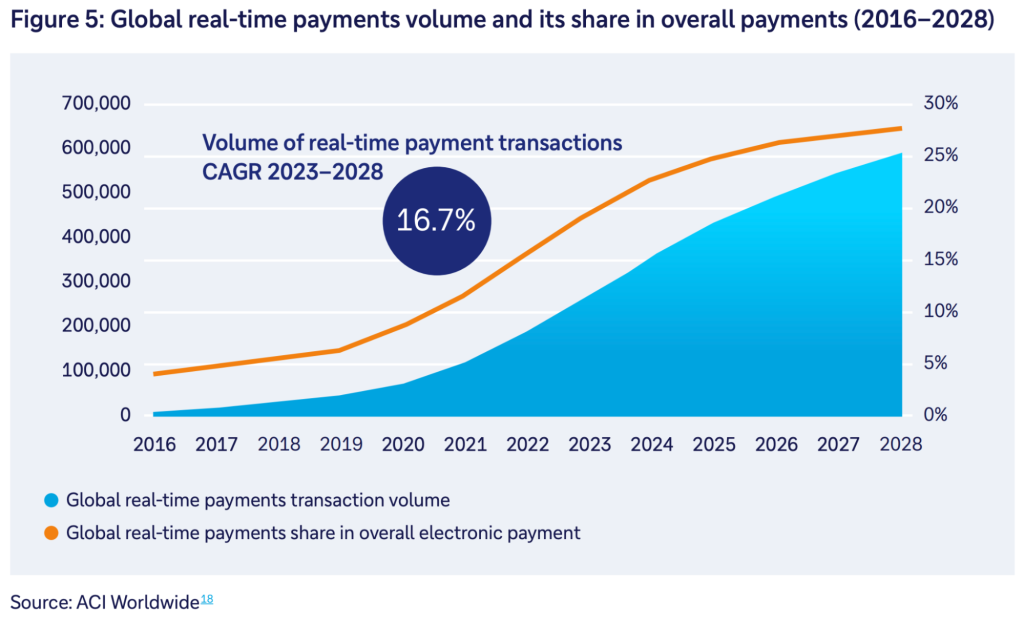

By 2028, real-time payments are expected to constitute 27.1% of all payments globally.

With two systems working side by side, each catering to different market segments, the potential to transform how money moves across the country is immense. Their rivalry pushes both to innovate, improve accessibility, and lower costs, while their eventual interoperability could lead to a unified system that benefits everyone

By 2028, RTP is expected to constitute 27.1% of all global payments. With this capability, international trade finance will be unrecognisable, dramatically reducing transaction times and increasing liquidity for businesses.

The journey will continue as these two systems learn to paradoxically coexist, compete, and ultimately work together to improve real-time payments for everyone.