Trade credit insurance (TCI) and surety play a vital role in the global economy, yet they are often overlooked. These instruments provide a safety net that allows businesses to navigate unpredictable financial landscapes more confidently, ensuring that their cash flow remains stable and contractual obligations are met.

In times of economic uncertainty, TCI and surety become even more crucial, fostering resilience and reducing the financial risks of doing business.

Examining the sector’s role in current times, the Swiss Re Institute has published its report titled, ‘Credit and surety in the age of economic uncertainty’.

If you don’t have time to read the full report, here are our five key takeaways.

1) TCI and surety support a resilient economy during times of uncertainty

TCI and surety are crucial in fostering resilience amid economic uncertainty, providing a safety net that allows businesses to navigate unpredictable financial landscapes more confidently.

TCI helps to ensure that a business’s cash flow remains stable by protecting companies against non-payment by their clients, a risk that increases amid the increased business defaults accompanying economic turbulence.

Surety bonds, conversely, provide a form of security that contractual obligations will be met or compensation provided if they are not. They are often used to safeguard large and high-stakes projects, such as those in the construction sector, and become ever more important during uncertain economic times when the risk of a party failing to meet their contractual commitments increases.

Both instruments share the common goal of reducing the financial risks of doing business, ultimately affording companies the confidence to continue investing, expanding, and hiring, even in less stable economic environments.

This continuation of business activity helps to mitigate the potential of a vicious reinforcing feedback loop of declining economic confidence and activity, which is something that has been gleaned from past crises.

2) Approaches to TCI and surety have been informed by past crises

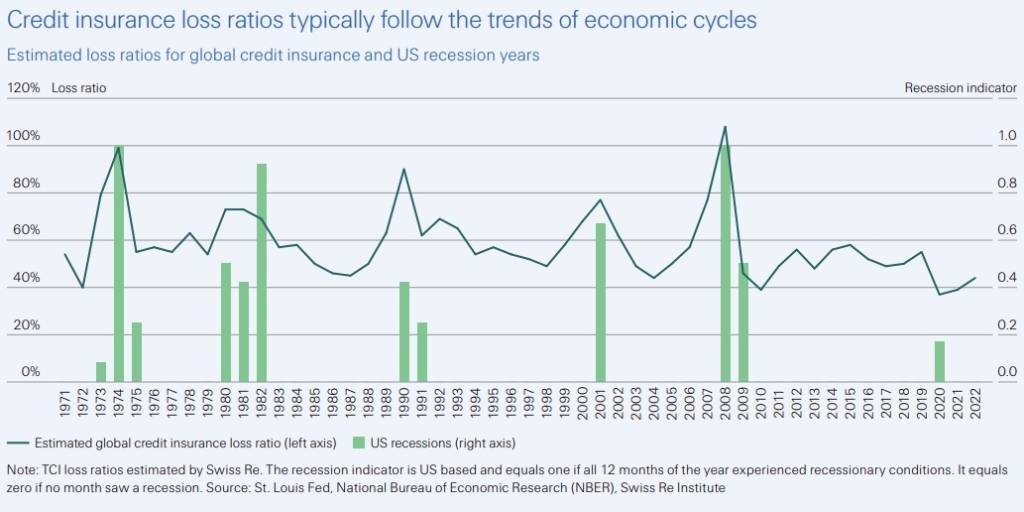

TCI and surety have evolved their strategies in response to past economic downturns, such as the global financial crisis and the COVID-19 pandemic, highlighting their close ties to the economic cycle and necessitating key operational adaptations.

For TCI, the global financial crisis underlined the necessity of limit adjustments and proactive risk management to mitigate losses. This experience informed the approach taken during the COVID-19 pandemic, where swift government interventions and state schemes helped maintain more stable TCI coverage compared to the financial crisis.

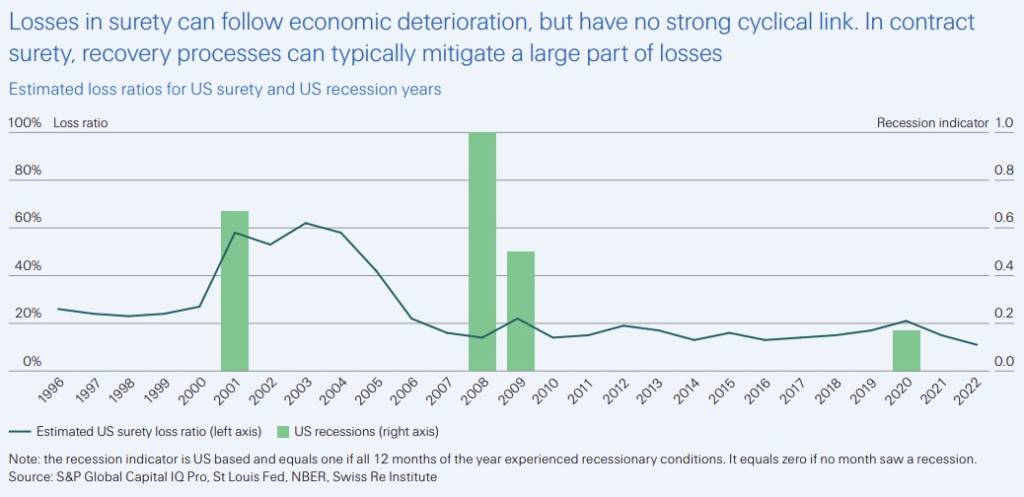

In the surety sector, these downturns have emphasised the complexity of its relationship with the economic cycle.

While surety claims are influenced by economic conditions, the lack of a direct link between the business cycle and loss ratios has necessitated a more nuanced approach to risk assessment and management.

Both sectors have learned to be more adaptable and responsive to changing economic conditions, enhancing their resilience and preparedness for future economic challenges.

3) Economic indicators point to troubles ahead

The Swiss Re report forecasts a global slowdown amid concerns that the economic outlook is weakening, particularly as the effects of monetary policy tightening begin to take hold.

While major economies have shown resilience thus far, that resilience is being tested by rising corporate insolvencies and bankruptcies, which are crucial determinants of loss frequency in the TCI and surety sectors.

Other key indicators include GDP growth, trade and manufacturing, inflation and interest rates, and public construction spending and output.

Of these, trade flows are experiencing high volatility, manufacturing activity has seen a downturn, inflation and interest rates are expected to remain elevated, and construction sectors in many key markets are confronted with short-to-medium-term challenges.

These economic conditions are expected to present stark challenges in the years ahead.

4) Growth opportunities remain despite challenges

Despite the economic challenges presented by the global economic environment, there are growth opportunities for trade credit insurers and surety companies.

As corporate insolvencies increase, there will be a growing demand for trade credit insurance as businesses seek protection against defaults in a more volatile environment. Additionally, the return of inflation, while adding complexity, has driven up the insured credit exposure, suggesting a broader market for trade credit insurance services.

In the surety sector, there are many opportunities related to large-scale infrastructure investments. A significant portion of the infrastructure planned to be built by 2040 is located in emerging markets, with India being highlighted as the second-largest emerging market for forecast infrastructure investment.

This focus on infrastructure in emerging markets offers new business opportunities and highlights the importance of maintaining relationships with contractors. By closely monitoring for early signs of financial distress, surety companies can better manage risks while providing a critical service for these large infrastructure projects.

Despite the economic headwinds, the ongoing demand for protection and the burgeoning infrastructure projects in emerging markets present robust opportunities for growth in both the trade credit insurance and surety sectors.

This growth may be aided by developments in digitalisation.

5) Digital development progressing, but more opportunities remain

The digital transformation journey in the credit insurance and surety sectors has seen significant progress, although the outcomes have not met expectations. Digitalisation promises to reduce costs and enhance efficiency for these financial services, and its impact has been strong over the past few years.

One of the technologies at the forefront of this transformation is artificial intelligence (AI), which has been instrumental in improving efficiency, particularly for trade credit insurers. However, such technology is used more by larger players in the field, indicating an adoption gap across different sizes of companies.

Other promising developments include digital platforms and blockchain technology, which both have the potential to enhance efficiency across the entire value chain. Insurers and insurtech companies have been developing platforms that target small and medium-sized enterprises (SMEs), a segment that still remains largely underserved.

The growth of the B2B platform economy presents additional opportunities for insurers. It could allow them to offer novel solutions, such as deferred payment options, which would be particularly appealing amid an uncertain economic landscape.

The Swiss Re Institute’s report on ‘Credit and surety in the age of economic uncertainty’ provides insights into the evolving dynamics of TCI and surety in today’s economic climate.

While the sector faces significant hurdles, including a global economic slowdown and rising corporate insolvencies, it also encounters unique growth opportunities, especially in emerging markets and through digital transformation.

The report highlights the important role of TCI and surety in sustaining global economic resilience, highlighting its adaptability and potential in navigating and capitalising on the complexities of the current financial landscape.