")

Before 2019, Sibos made its last appearance in the UK in Brighton, 1985. So, what was the world like in 1985?

Sibos 1985 (Brighton, UK)

What was the world like in 1985? Things were quite different. The average house would set you back £40,000, interest rates for the Bank of England were 11%, and the film: Back to Future was released.

On the tech front, the UK made its first mobile phone call, Microsoft released the first version of Windows, and the first .com domain name was released (symbolics.com).

Sibos 2019 (London, UK)

Fast forward 34 years and the world’s trading system has been substantially impacted by many factors, from the impending exit of Britain from the European Union to the tit-for-tat behaviour and increasing escalations of China and USA.

Such factors, some have argued, have always been present throughout the last century or so.

As a global trading platform, the overall consensus has shifted considerably. What was once a picture-perfect idea of specialisation and economic growth, is now in reality, a rise in nationalism and the apparent desire to protect one’s own domestic produce.

But how have some of these international political disputes affected trade; and more specifically the environment for which trade finance operates within? Following on from Sibos 2019, we’ve put together our thoughts on the major events and how the outlook and landscape for trade is changing, as well as the current initiatives which are progressing to make upgrade trade finance in the same style we’ve seen Windows grow from 1.0 to 10.

Trade Wars & Soybeans

The deterioration of the political relationship between the US and China has been a substantial contributor to the current climate of ever-rising product and country-wide tariffs, and ever-falling volumes of trade.

So far in this saga, the US has implemented tariffs on approximately $550 billion worth of Chinese products. On the contrary, China has implemented tariffs on around $185 billion worth of US goods. Although there have been multiple talks between the two monoliths, neither side seem to have agreed a way of withdrawing from tariffs now set in place.

There have, in result been reductions in the tariffs (exemptions – a formal notification from the US Trade Representative that withdraws the specified products from any tariff charges). More recently, on the 20th September they released a notification in which exemptions were granted for over 300 products, which varied from Heat exchangers, all the way to anaesthesia masks.

This was met with grace, with the Chinese issuing exemptions for multiple domestic companies to purchase American Soybeans without being subject to the tariffs implemented in retaliation to American Tariffs. This polite ‘nod’ is a positive sign, but unfortunately is not yet reaping the benefits.

On the above chart, we can see directly the lag in the actualisation of good-will exemptions, as on Monday – the day China announced the Soybean relief – the price rose 0.2% from 892.5 to 894.25 and has since fell 0.5% to 889.25.

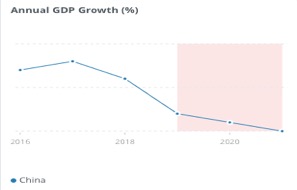

If we are to look toward Chinese Annual GDP Growth (%), we can understand that as an economy China was slowing down – this was no secret. The levels of exponential growth the country experienced were critical in their place in today’s trading world, but by no means sustainable.

2017-2018 saw the first real decline in GDP growth (%) since the turn of the century, with it falling 0.2% to 6.6%, May 22nd, 2018, Trump signed the first trade-war-style tariffs on product industries such as aerospace, IT and machinery. If we look at 2018-2019, we can see the considerable decline in Chinese GDP growth, falling from 6.6% down to 6.2%.

Trade Outlook

On-going trade tensions that have tightened, then loosened and so on, are creating a complex environment for businesses to be trading in. Many media outlets have reported on forecasts of the worst global economic growth since the financial crash of 2008, or the fact that the volume of global trade has actually declined in the first half of 2019 for the first time since 2009.

Back in April, WTO Director-General Roberto Azevedo said

“Trade cannot play its full role in driving growth when we see such high levels of uncertainty. It is increasingly urgent that we resolve tensions and focus on charting a positive path forward for global trade which responds to the real challenges in today’s economy”.

Roberto Azevedo, WTO Director-General

However, we must remember trade wars really aren’t anything new. Perhaps the scale of today’s is far different, but the concepts are no different. If we look back into previous increases of international uncertainty created by behaviour typically associated with ‘trade wars’, we actually see that the demand for Trade Finance increases, so it may not be all bad.

Silver Lining

In order to understand the real opportunity that presents itself, we must first understand how the world re-directs demand in response to these trade wars. With China suffering significantly from the monumental number of tariffs, the possibility of manufacturing units that once flocked to China for their competitive corporate environment and associated advantages, may now be faced with the option of moving operation elsewhere. The essence of this has already begun, with nations – specifically Vietnam – picking up excess demand that the Chinese lost due to higher costs experienced due to tariffs. Vietnam in particular is an interesting case, as we heard at FCI’s Annual Conference in Ho Chi Minh City. They are accounting for so much of the previous-Chinese demand, that they too are now at risk of facing US tariffs.

Vietnam is doing what it can to seize the sudden boom that has been generated from the increasing tensions between the US and China. It is almost stuck between a rock and a hard place, because on the one hand they want to make the most of this opportunity (export as much as possible, and increase resources to provide this), but don’t want to risk then becoming a target for the US to tariff, especially given the level of the US’ latest charges.

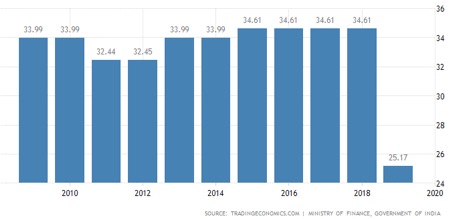

Another country that is not to be excluded from the list of replacements is India. Recently the Indian government has boldly moved to drop its corporate tax rate by -27% from 34.61% down to 25.17%, in a bid to encourage corporate interest in the nation – quite the timing.

So how does Trade Finance benefit from this? By facilitating the deficit of trust that exists within the process of setting up and acting upon new international trading relationships. This can be seen with Mexico, for example. For the past few decades, Mexico has essentially relied on the US for exporting and importing, with their northern neighbours accounting for 51% of Mexico’s total imports, and a weighty 73% of total Mexican exports in 2017 (World Bank).

Mexico is now having to look to Latin America, to Africa and to Asia for new trading channels, and what this means for Trade Financers is a massive opportunity to provide new finance to these emerging markets. More importantly they must nurture and facilitate trust between active parties within the new agreements that will inevitably be made.

Once the agents within these emerging economies have been identified, it is then a question of ensuring they receive competitive rates on the working capital finance they are offered in order to protect long-term trading behaviours/ relations. This is something many financiers are currently looking into as the world’s trading patterns change.

Unseen Uncertainty

Multiple institutions have reported feelings of great uncertainty from their clients, and it is clear to see in the market too. This is a very turbulent time politically, and economically. There is, of course the US/ China trade war; there is then the fiasco that is Brexit; there is also the political crisis experienced in Hong Kong, with mass protests demanding deeper democracy as their independence from China is threatened.

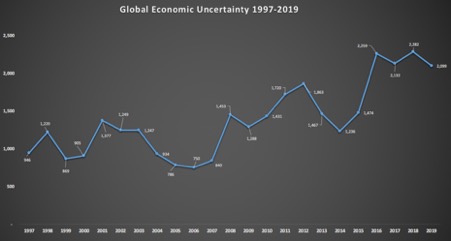

Uncertainty is a term that everyone is familiar with by now, but if we look back over the past 20 years or so, how does today’s uncertainty measure up?

There exists an Economic Policy Uncertainty Index, funded by the Stanford Institute amongst others for Economic Policy Research. The index uses something called EPUM criteria to search newspaper articles that satisfy the required criteria:

- E: Economic, Economy

- P: Congress, Legislation, White House, Regulation, Federal Reserve, Deficit

- U: Uncertain, uncertainty

- M: Federal reserve, the fed, money supply, open market operations, quantitative easing, monetary policy, fed funds rate, overnight lending rate, Bernanke, Volker, Greenspan, central bank, interest rates, fed chairman, fed chair, lender of last resort, discount window, European Central Bank, ECB, Bank of England, Bank of Japan, BOJ, Bank of China, Bundesbank, Bank of France, Bank of Italy

Based on the latest data from the Economic Policy Uncertainty, the Baker Bloom & Davis Index shows us the frequency of the above terms in today’s media is considerably higher. Sitting at an index of 2,099, it is 45% higher – more uncertain – than it was in 2008. For more information on the mathematical methods used to calculate the above, click here.

Technology’s place

Following the massive entrance of Bitcoin in January of 2009, the world has been introduced to the possibilities of blockchain, across all industries – specifically Trade Finance. With the very nature of Bitcoin being security and transparency, the application of this to Trade Finance is set to revolutionise the way in which cross-border trade is facilitated.

There are now great players at the front of the industry, pushing the technological abilities of the ecosystem. Players such as We.Trade, Deutsche Bank, Komgo are all part of a first-class system of banking institutions, consortiums and active businesses all active within the market of blockchain.

Back to the Future

The above technology will indefinitely have monumental effects on the way the world trades, and subsequently the way we finance said trade. But what will come of the on-going political disputes currently shaking the playing field upon which the world trades.

The number of firms operating today that offer Blockchain solutions are astounding compared to even 5 years ago. Company’s such as Vakt, who connects key players to trades within the oil industry, or Voltron, a coalition of over 50 banks which use block-chain like technology to fulfil end-to-end L/C’s.

A turbulent time it has indeed been, but there are important events on the horizon which could put an end to the chaos. The US presidency is due for renewal in 2020, and although Trump is running again, the possibility of a candidate with a less aggressive approach to trading measures would certainly be a breath of fresh air for many. On the other hand, an agreement between the two parties may happen at some point, the question is how much longer it must go on for.

With regards to Brexit, the complications surrounding the entire process from day one has resulted in an equally foggy environment in which businesses are faced to prepare for an outcome, they can’t identify. With the latest unlawful prorogation of parliament, the impending date of October 31st – the promised leave date of PM Johnson – the Prime Minister is faced with difficult times, and his delivery of Brexit – more specifically the way in which it is delivered is unknown, and presents a challenging environment for UK trade.

However, Brexit will happen as it was the democratic decision of the people of the United Kingdom. The US may get a new president or may retain Trump and possibly reach a deal. Emerging economies such as Vietnam and India may begin/continue to take a larger percentage of world trade, all the while creating new channels of trade and thus, opportunities for trade finance.

Trade in a new era

TFG have partnered up with the World Trade Symposium to continue the discussion around geopolitics, policy and trade. Hear the latest from world experts in New York in November.