Global Credit Data releases extensive analytics on loss given default, including the first complete account of losses from the 2008 financial crisis

As banks deal with the ongoing consequences of Covid-19 on the global economy, Global Credit Data (GCD) has published its 2020 report on Loss Given Default (LGD), offering the latest numerical evidence of recoveries and losses incurred by banks from loans to large corporate borrowers. The report is based on a clear and qualified set of data, underpinned by verified, high-quality information collected over 15 years from more than 60 global and regional banks.

“While it is difficult to assess the precise implications of the current Covid-19 epidemic on the global financial system and on bank losses, today’s historical LGD analytics offer invaluable and detailed data for banks to train and adapt their existing models,” says Richard Crecel, Executive Director, GCD.

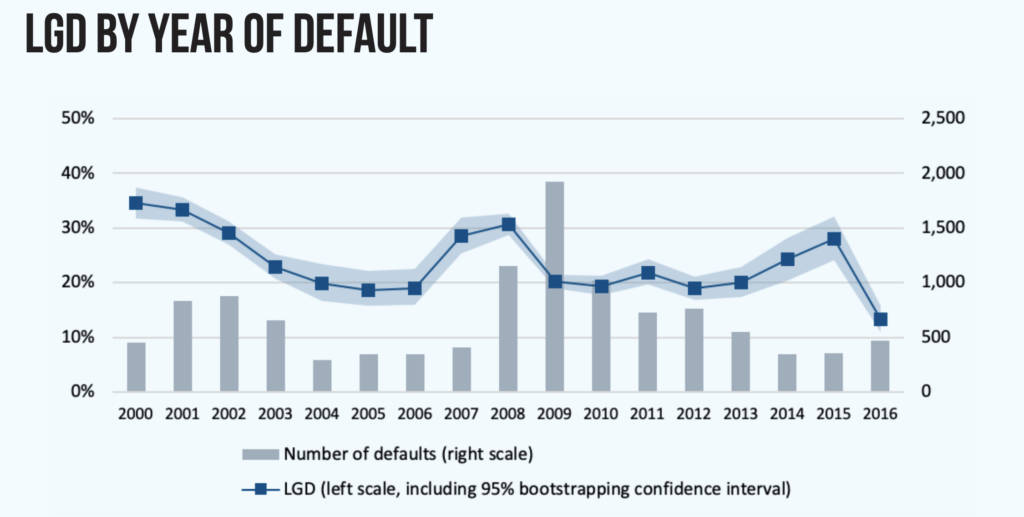

GCD’s LGD report represents the industry standard for collecting, reporting and benchmarking bank’s credit risk data and this year’s edition represents the first complete account of the losses incurred during the global financial crisis of 2008.

“These latest results not only represent a full account of the losses incurred in two crisis periods, but also demonstrate remarkable consistency over time – indicating the robustness and reliability of our historical data set,” says Nina Brumma, Head of Analytics and Research at GCD. “The insights gained from these high-level analyses confirm the benefits of detailed and granular collection of post-default cash-flow data – critical for banks as they navigate the current crisis.”

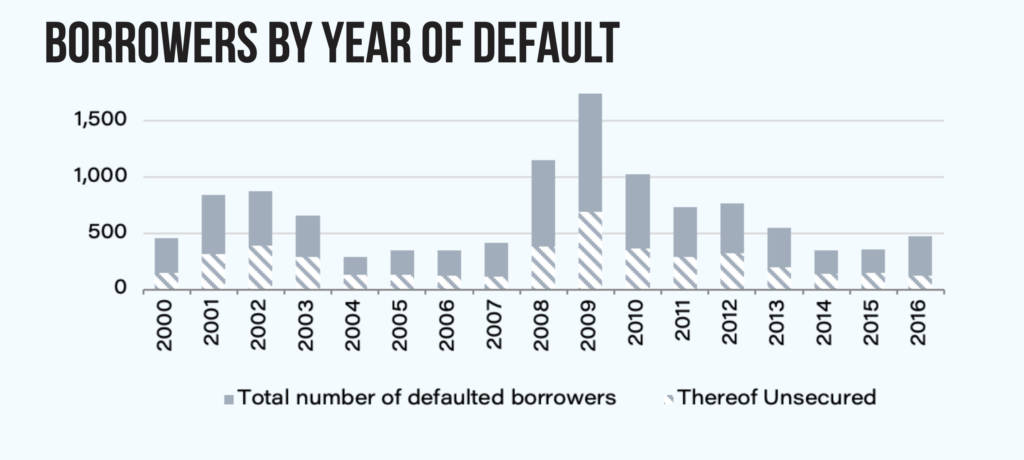

LGD data takes many years to fully mature, since recovery processes take a while to start (allowing for delayed payments on the original loan) and longer to work out (collateral, for instance, must be acquired and then sold at an acceptable price, or senior debt must be repaid through liquidation processes in the case of administration). After years of collection and curation, however, data from the financial crisis has finally matured, offering industry participants a timely and comprehensive toolbox to extract and understand loss levels and engage in an informed dialogue with regulatory bodies in light of the current pandemic.

Given the difficulties in translating observed losses into accurate predictions of future losses, it is critical for banks to continuously develop and refine their models – a process that must be underpinned by large, high-quality data sets.

“The benchmarking of credit risk data is more important than ever to support banks in coming to a more sophisticated understanding of the crisis impact,” Crecel concludes. “This will ensure not only a better response to the current situation, but, through consistent monitoring, sharing and benchmarking of loss data, put banks in a better position to adapt to future crises.”

What is Loss Given Default?

Loss given default (LGD) reflects how much money a bank or other financial institution loses when a borrower defaults on a loan, expressed as a percentage of total exposure at the time of default. LGD is one of the key factors used to calculate expected credit losses, along with probability of default (PD) and exposure at default (EAD).

Now launched! Summer Edition 2020

Trade Finance Global’s latest edition of Trade Finance Talks is now out!

This summer 2020 edition, entitled ‘Coronavirus & The Fourth Industrial Revolution’, is available for free online, covering the latest in trade, export credit insurance, receivables and supply chain, with special features on fintech and digitisation.