With the development of more interconnected alternative finance options for businesses and the emergence of open banking in the marketplace, the option of Peer-to-Peer (P2P) lending is seeing a great increase in popularity over the years among its SME audience.

However, P2P Lending firms have recently been facing some issues and in many cases, closure even among our ever interconnected economy. Many SMEs and prospective investors are left wondering if P2P lending is really the best route for alternative financing.

By the people, for the people

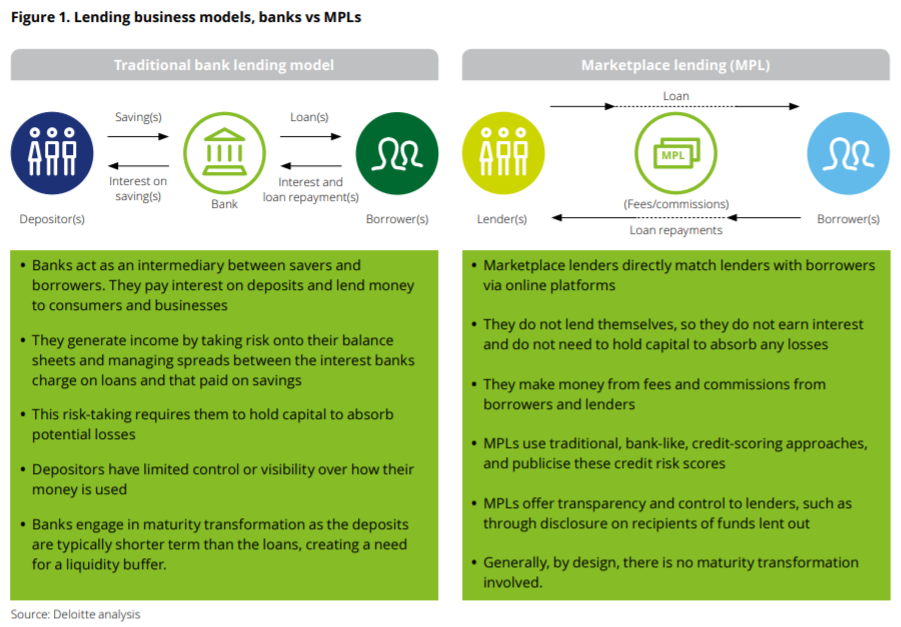

P2P lending, otherwise often known as marketplace lending, is an alternative finance option mainly catered to SMEs and those looking for specialized loans facilitated outside of conventional banking institutions.

- P2P lending takes place the online marketplace, connecting borrowers to investors directly without intermediation

- Lender profiles are often of individual investors looking for better cash savings returns compared to what banks offer

- Borrowers seek to benefit from easier access to loans at decent rates

- Popular P2P lending platforms include: Upstart, Funding Circle, Prosper Marketplace

- Most host sites possess a variety of interest rates, evaluated on applicant creditworthiness

P2P hosts generate revenue through borrower-side origination fees, and from investor-side interest and service charges.

Lending Business Models: Banks vs P2P Lending (MPL).Source – Deloitte Analysis

But P2P still looks to rise up in the ever-evolving Fintech world; in a PriceWaterhouseCoopers report, they estimate that “the [P2P lending] market could reach $150 billion or higher by 2025.”

However, due to this nature of P2P Lending framework, the practice is subject to a level of risk and need for regulation, something platforms in China have been expressly struggling within recent times.

The Current Landscape: Risk and Regulation

China: Rapid growth, Failing Fast

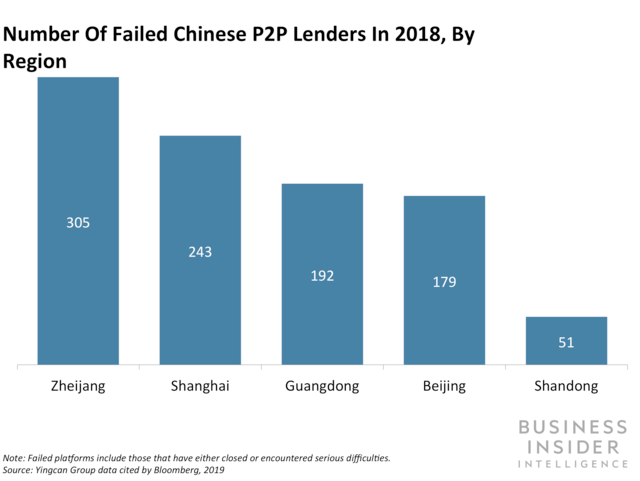

With the most recent victim being Locaibao.com, one of the Shanghai-based investment firm Zendai‘s P2P lending platforms, pulling out of the P2P industry this August, the Chinese crack-down on regulating P2P platforms have seen more than 80% of its once totalling 6200 platforms closed or shutdown.

Number of P2P Platforms shutdown or pulled out by Chinese regulators. Source – Business Insider

In the beginning, P2P lending gained rapid popularity in Chinese markets due to its ability to fill the gap in the country’s underdeveloped consumer credit market, and due to the country’s high savings tendencies (46%, one of the highest in the world according to McKinsey studies).

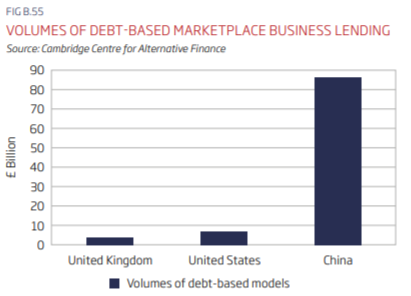

China still leads in P2P lending amongst UK and US markets. Source – British Business Bank (BBB), Small Business Finance Report 2019

“Zendai’s collapse is an indication of an industry that grew too far and too fast in the wrong direction. The Chinese P2P market was one plagued by misappropriation of funds, dubious lending standards, and outright fraud. This current implosion should be a stark lesson for regulators in other markets as they seek to regulate and rein in what is often becoming an out of control segment.”

— Zennon Kapron, founder and director at Kapronasia

Initially P2P lending faced a more hands-off approach from regulators, and this lack of oversight resulted in skyrocketing industry growth, with outstanding marketplace loans in the country starting from almost zero in 2012, up to 1.22 trillion yuan ($176 billion) in 2017.

Now with the eruption of fraud and victims stepping out into the spotlight, action has undoubtedly been taken by the China Banking Regulatory Commission to clamp down on P2P regulation. Much of the 80% shutdown were said to be due to the implementation of fraudulent schemes or poor investment decisions. Thus causing the closure of platforms hosting more than 1.5 million clients consisting of 112 billion yuan ($15 billion) of loans outstanding.

“This is why it went wrong.”

Some believe regulation was not the right route in cracking down on P2P lenders.

“An industry that should have been regulated more was not, and now we’re seeing that implode with even the stronger players […] pulling out of the industry”

— Zennon Kapron, founder and director at Kapronasia

An anonymous banking regulator source from a Reuters report commented that “[t]he problem was, there was no time to do the analysis, […] The authorities had no toolbox to supervise the firms; there was no offsite surveillance,” and that, “This is why it all went wrong.”

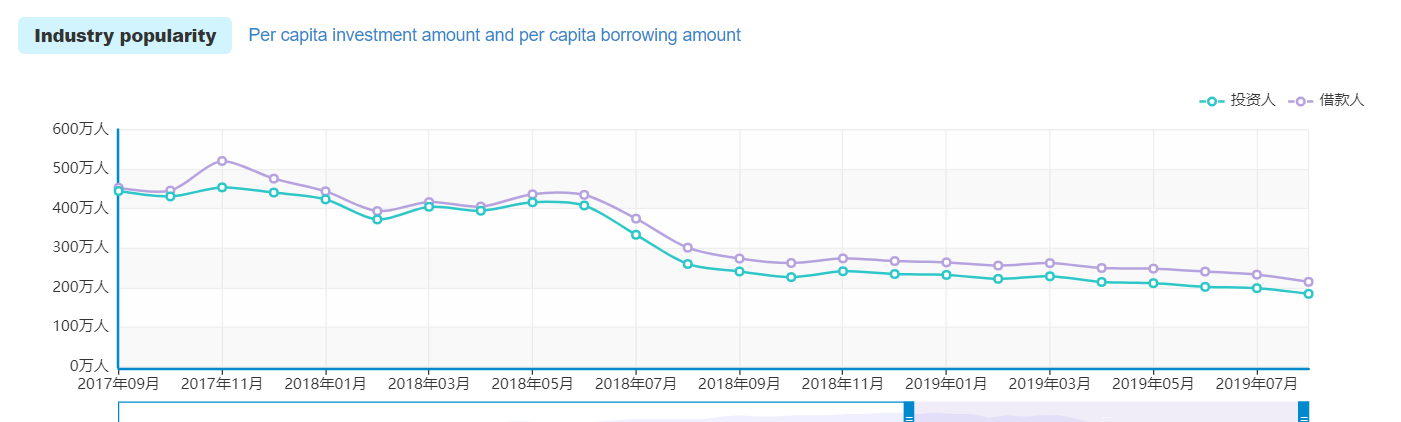

The declining popularity of the P2P lending industry in China, September 2017-August 2019. (Green – Investor Population / Purple – Lender Population) Source: Wangdaizhijia

In recent numbers of this August, the number of active lending decreased by 7.20% from the previous month (by 143,700) and the number of active borrowers decreased by 7.79% (by 182,100).

However, many others also identified gaps in the P2P lending market as problems rooted in the industry’s lack of public awareness and trust.

UK: A Conflict of Trust and Growth

Some blockchain analysts believe P2P platforms are faced with the conflict with building trust and growth at the same time: as a network grows, the bigger the risk pool and the less trust users often place in it, but simultaneously, platform growth is essential to growing a profitable performance of the P2P platform.

McKinsey commented that the “P2P mania also attracted a number of less scrupulous players that created P2P lending platforms simply as a fast and convenient channel to raise short-term funding from individual investors.”

The trick is to build meaningful awareness in trustworthy sources, balancing the two goals in platform marketing strategies.

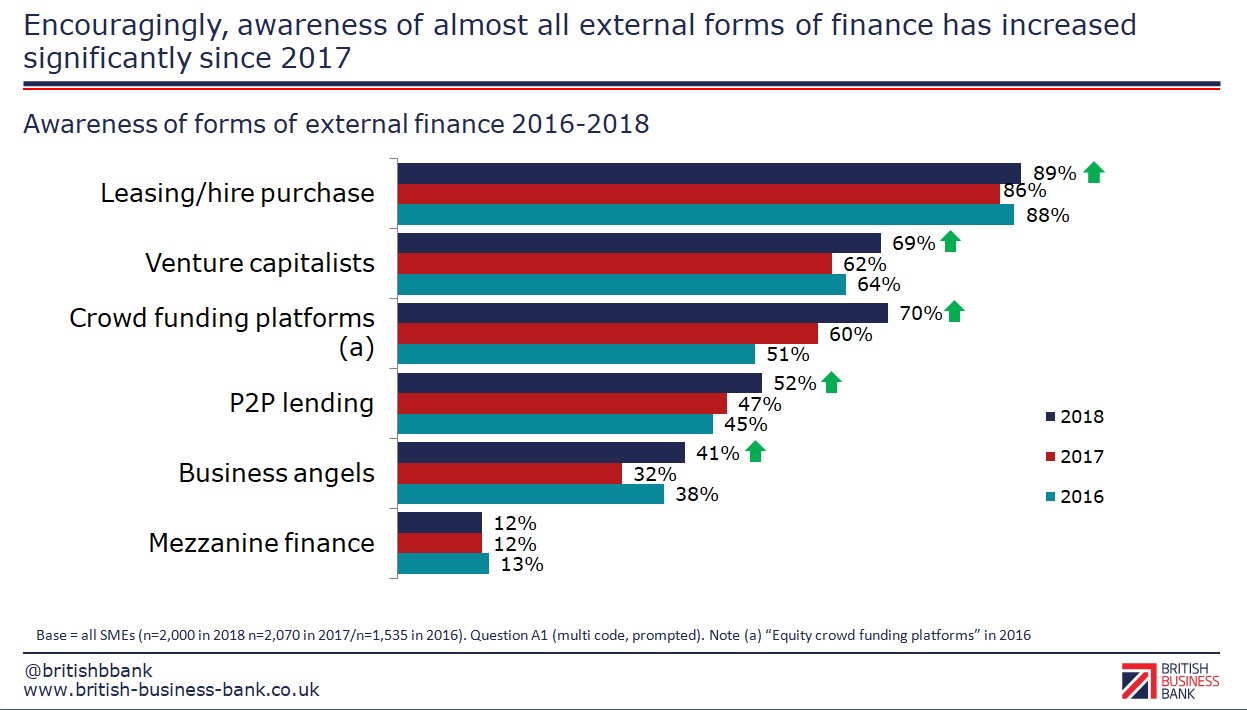

Growth in awareness of alternative financing, including P2P Lending (up 41%, 2018) in the UK. Source – British Business Bank (BBB), Small Business Finance Report 2019

But especially with the recent regulatory sweep in China that cost thousands of P2P platform shutdowns, growth in both trust and awareness have experienced major hiccups in the past year.

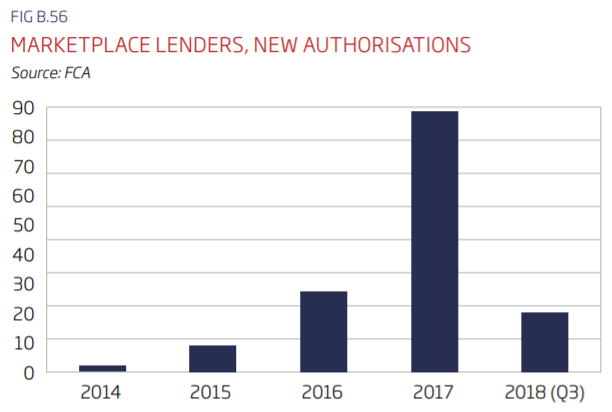

2018 sees a drop in new P2P platforms in the UK. Source – British Business Bank (BBB), Small Business Finance Report 2019

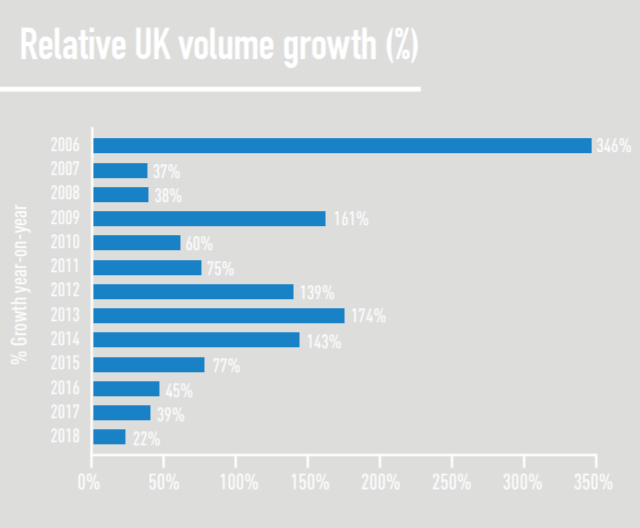

UK P2P Engagement Growth slows down to 22% in 2018. Source – AltFi Report

In response to the slowing growth and the increasing untrustworthiness of P2P lending, the financial regulatory body in the UK, Financial Conduct Authority (FCA) has produced policies regarding new restrictions on the marketing of P2P platforms April of this year.

The FCA identified the platforms to harbour high-risk investments, that should be carefully considered by borrowers and lenders.

The FCA enforced that P2P platforms must only market to clients that…

- Are certified as “sophisticated investors” / “high net worth investors”

- Receive regulated investment advice or accredited investment management service

- Are certified as “restricted investors” (will not invest over 10% of net investable assets in the P2P platform)

Although these regulations seem to address the issue of controlling the riskiness of investments and encourage trust, many P2P platforms disagreed with the policy.

P2P platforms were concerned that the FCA rules would…

- Restrict lending to sophisticated investors and thus destroy the “point” of P2P lending, and perhaps kill the industry itself

- Give a misleading impression of the risk of P2P investment and discourage involvement

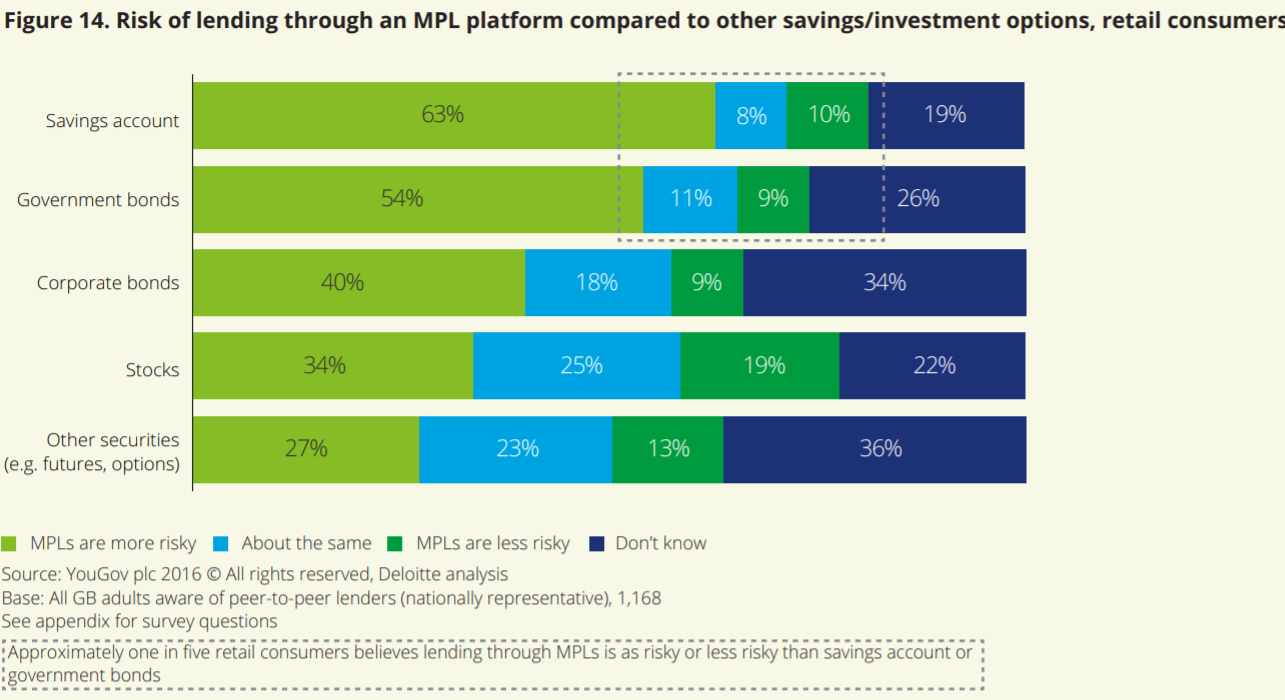

According to a survey by Deloitte, one in five retail consumers believes P2P Lending is as or less risky than savings accounts or government bonds. Source – Deloitte report

However, no matter the marketing strategy, costs in marketing prove to be a major issue with platforms, with one of the US’s leading platforms, Lending Club, even through achieving $3.1bn loans (2018 Q3) still delivered a small net loss, with high marketing expenses taking up more than a third of their revenue.

Platforms going forward should learn from the downfalls many peers have experienced in the 2018-2019 period, and in the words of Rhydian Lewis, chief executive of the UK-based P2P RateSetter, “It means not reaching too hard for high returns, which will become high losses in a recession. It means sticking to niches with good borrowers, who are too hard for big banks to serve. Finally, it means not spending excessively on marketing.”

Looking back, moving forward

As always with all alternative finance opportunities are sprouting, but understanding the behaviour and failures of alternative funding like P2P is crucial in weathering the storm, especially when the risks are high.

Many believe slow and steady growth in awareness and trust will prove to be a sustainable path to profit in the P2P lending industry, rather than following the rapid growth and fall of many Chinese lending platforms.

In a previous TFG article, future predictions of the P2P industry marked a timeline of the quality of the industry, and one year on, the industry is recovering from the “trough of disillusionment”.

Learning from the platform shutdowns and leveraging what P2P holds as competitive advantages is crucial in moving forward in the alternative finance industry.

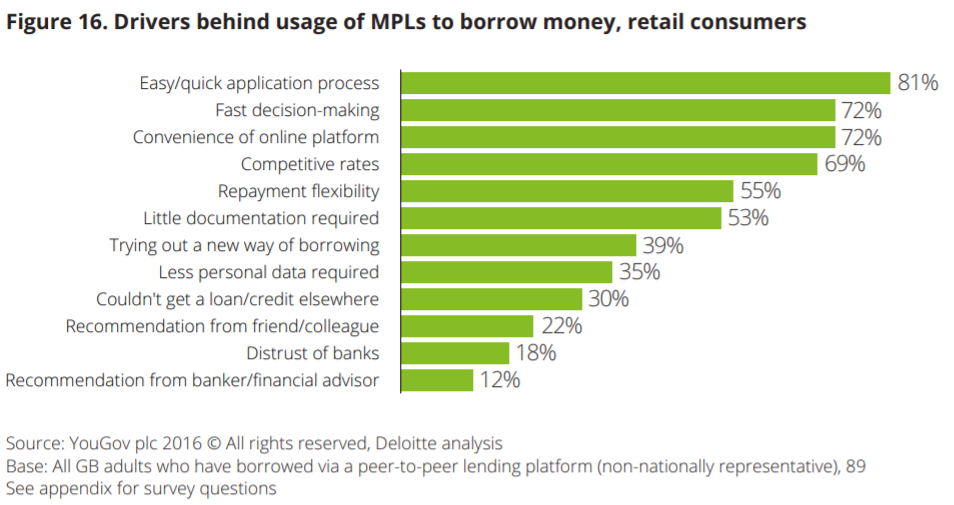

The top determining factors in choosing P2P Lending (MPL) by retail customers. Source – Deloitte report

Balancing regulation and innovation has historically been difficult to weather, but with examples all over the world from China to the UK, the P2P lending industry has the opportunity to learn and anticipate for the opportunities and challenges of the near future.

Want to find out more about digital trends in the alternative and receivables finance? TFG has partnered up with BCR at both their Alternative & Receivables Finance Forum and Masterclass in November.